This year’s federal Budget which was handed down on Tuesday 6 October has been designed to kick start the economy, create jobs and encourage spending.

The Budget reforms have had a positive impact on two areas of estate planning – namely Testamentary Discretionary Trusts (TDTs) and Granny flat arrangements.

Tax Impact on TDTs

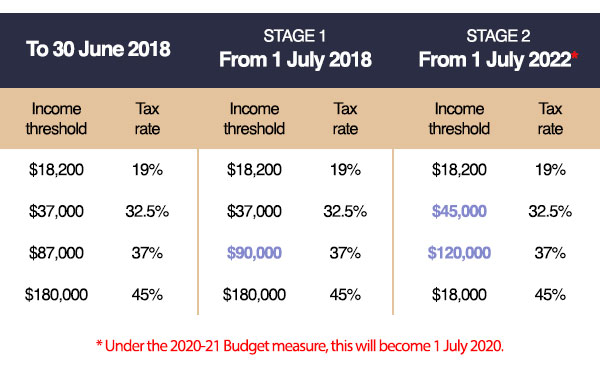

The reduction in the personal income tax rates means that TDTs are now an even more tax effective vehicle to store inheritances. The Stage 2 changes to personal income tax rates has been moved forward 2 years and will now start from 1 July 2020. What this means is that trust income distributed to minors or in fact any adult beneficiary will be taxed more effectively for the 2020/21 financial year and onwards.

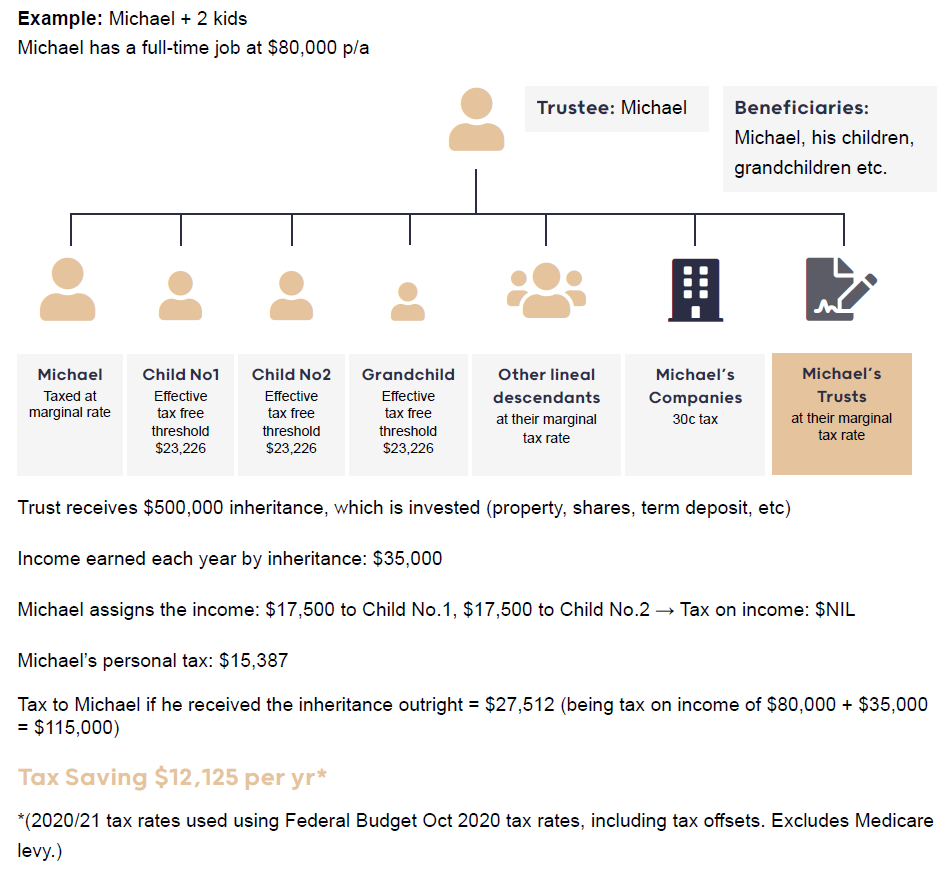

As a quick refresher, a TDT is a trust that you establish in your Will for the benefit of your family or other loved ones. TDTs are popular in Wills because they provide significant tax opportunities as well as asset protection benefits that providing an inheritance direct to a beneficiary do not.

The following table summarises the changes to the various tax thresholds. The tax saving for low income earning beneficiaries of the TDT have further been enhanced by the increase in the low income tax offset (LITO). This is particularly effective for children under 18 who are beneficiaries in the TDT.

TABLE 1: Summary of individual income tax rates – residents

These changes mean that the trustee of a TDT (the controller) can assign trust income to beneficiaries who will pay tax at these new marginal rates.

It is also important to remember that a TDT allows minor beneficiaries (such as young children/grandchildren) to be taxed at adult rates (with a tax free threshold of $23,226 per year) as opposed to the tax rates for minors receiving trust income in a family trust (namely a trust not in the Will) which has a tax free threshold of only $416 per year.

Please note that these changes are subject to the bill receiving royal assent. For more information on the effectiveness of TDTs and examples of how the tax concessions work, please see our factsheets here.

If you would like to include TDTs in your Will or have any questions on your estate planning, please contact us.

Granny Flat Arrangements and Capital Gains Tax

Under the current law, a homeowner may be liable to pay CGT where there is a formal agreement with a family member (often an elderly parent) who resides in their home.

Example:

An elderly parent pays their homeowner daughter $300,000 to build a granny flat on the understanding that the older person will have this amount repaid to them if they exit or paid to their estate if they pass away. This results in a taxable gain of $300,000 to the daughter with no CGT concession.

If the parent instead pays the daughter rent, this is assessable income for the daughter and results in a partial loss of the CGT main residence exemption.

The Government has announced that it will provide a targeted capital gains tax (CGT) exemption for granny flats provided that there is a formal agreement in place.

One of the most common forms of financial elder abuse that we see in the emerging case law relates to granny flat disputes, where one party wishes to exit the arrangement. In fact, a 2019 review found that:

“‘Informal’ granny flat arrangements, based on concepts of trust and ‘natural love and affection’ present real risks to the older person residing in the granny flat.”

Board of taxation Review – November 2019

Under the measure, CGT will not apply to the creation, variation or termination of a formal written granny flat arrangement. This will remove the adverse tax consequences for the property owner while providing protection for older parents or people with disabilities.

The CGT exemption will be available only in respect of a granny flat interest within the meaning of s 12A of the Social Security Act 1991. The exemption will not be available for a property that is not the principal home (as defined in s 11A of the Social Security Act 1991) of the taxpayer (for example, a rental property that happens to contain a granny flat).

Please note that the changes have not yet been enacted. Also, the proposed changes remain silent on the issue of regular rental payments and whether that loses part of the CGT main residence exemption for a homeowner.

At Estate First, we can assist you with advice regarding co habitation (granny flat) arrangements as part of your overall estate planning considerations. We strongly recommend that if you are contemplating an arrangement with your children or parent, that you seek legal advice.

Stay in touch with us

Here at Estate First, your clients’ estate planning is our passion and focus. We value our working relationships with you as advisors and can support you in whatever way you need, including training and presentations (whether to your team or to your clients), compliance support, and tools and fact sheets (which you can use or provide to your clients). Please get in touch with us today by clicking here.